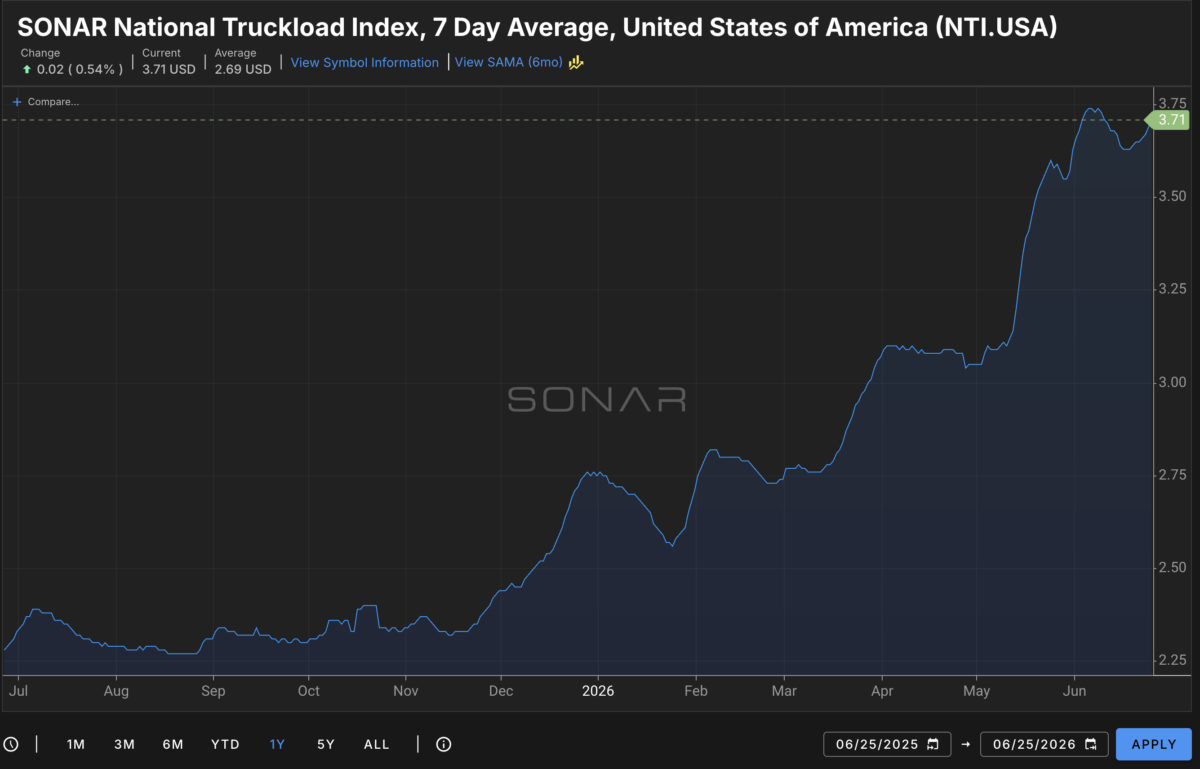

Now the market turns. Spot rates in mid-2026 are running roughly 15% above where they sat a year ago, the strongest year-over-year comparison since early 2022. That load that paid $2,200 last year is paying $2,500 or $2,600 now. Good. Real money. But there is a caveat, because this is where operators fool themselves. The diesel still costs what diesel costs, the truck payment did not change, the insurance did not drop a cent, and you are still waiting 35 to 40 days for the check (unless you are factoring). A bigger number at the end of a 35-day wait beats a smaller one. It is not the same thing as having cash this week, and it is not the same thing as running a healthy operation.

Here is the bigger picture. A high rate hides a bad operation, it does not fix one. When the market is hot, the operator with a bloated breakeven cost per mile and sloppy habits still makes money, so he never feels the problem. Then the market cools, the rate drops back toward his break-even, and the same decisions that were invisible at $2.60 a mile put him out of business at $2.20. The rate bought him time. It did not buy him a business. The operators who use a strong market to fix their cost structure are the ones still standing when it turns. The ones who use it to outrun their own decisions are just running up a bigger tab for later.

The Cost Stack That Showed Up Before the Rates Did

Here is what makes this market specifically dangerous. The costs the industry absorbed grinding through 2023 and 2024 never came back down, and the latest hard numbers prove it.

ATRI’s 2025 Operational Costs of Trucking report, the most authoritative cost benchmark in the industry, put the average all-in cost to run a truck at $2.26 per mile in 2024. Back fuel out and the marginal cost hit $1.78 per mile, the highest non-fuel operating cost ATRI has ever recorded. The cost of everything except diesel set an all-time record. Fuel coming down a little masked the fact that the real cost of running a truck kept climbing underneath.

Look at where the money actually went in that report, because this is where the playbook starts. Truck and trailer payments hit a record $0.39 per mile, up 8.3% in a single year and up 52.3% since 2019, a line item ATRI said had no equal for radical cost upheaval. Driver wages ran $0.78 per mile and total driver compensation, wages plus benefits, reached $0.97 per mile. Repair and maintenance sat just under $0.20 per mile and, after dipping in 2024, started climbing again in early 2025 as tariffs pushed parts prices up. And the truckload sector posted an average operating margin of negative 2.3% in 2024, meaning the average truckload carrier lost money on every mile. That is the cost structure you are carrying into this recovery whether you have measured it or not.

The Two Line Items Proving the Point: Labor and Insurance

If you want the clearest evidence that a hot market does not hand you profit, look at the two cost categories that keep climbing no matter what rates do: labor and insurance. Neither one cares what your settlement says.

Start with labor, because it is the largest single cost in the whole operation. ATRI put total driver compensation at $0.97 per mile, with wages alone at $0.78. The Bureau of Labor Statistics has truck transportation wages running above $30 per hour over the past year, and the pressure is not letting up. With new CDL restrictions and English-language proficiency enforcement projected to pull a significant number of drivers out of the qualified pool, wage pressure stays elevated heading through 2026. For an owner-operator, this cuts two ways. If you drive your own truck, your labor cost is your own pay, and the question becomes whether the rate actually leaves you a real wage after every other cost is covered, or whether you are just paying yourself last and calling the leftovers profit. If you run drivers, their pay is rising whether or not your rates rise with it, and a hot market that pushes driver wages up while you are locked into older freight rates squeezes you from both ends.

Now insurance, which is the cost that most cleanly destroys the “high rates mean profit” myth, because it has gone up every year regardless of the freight market, regardless of your safety record, and regardless of whether crashes went up or down. ATRI’s data put insurance at a record $0.10 per mile in 2024, up 3% after a 12.5% jump the year before. Zoom out and liability premiums rose 18.6% from 2021 to 2024, outpacing consumer inflation by 5.4 percentage points, while over that exact same window heavy-truck crash rates actually fell 2.6%. Crashes went down and your insurance went up, because the cost is being driven by litigation, not by your driving. Nuclear verdicts, jury awards over $10 million, surged 52% in 2024 to 135 cases totaling $31.3 billion, and the median nuclear verdict climbed to $51 million, up from $21 million in 2020. Commercial auto premiums rose 8.8% in Q2 2025 alone. And there is a federal proposal on the table to raise the minimum liability requirement from $750,000 to $2 million, which would push premiums higher still for exactly the small operators reading this.

Here is the part that should make every operator sit up. A new-authority owner-operator pays far more for insurance than an established one, and where you are domiciled (based out of) swings it by over $1,400 a month, from around $296 in Mississippi to $1,730 in New Jersey for the same operator. None of that is in your control on a load-by-load basis, and none of it goes down because the load board got hot. Your insurance bill arrives the first of the month at the same number whether you grossed $8,000 that week or $3,000. That is the definition of a cost that a high rate does not fix.

Now layer fuel on top, and this is where June 2026 gets ugly. The Iran conflict sent diesel up nearly a dollar a gallon in a single week back in March, and it never came back to where it started. As of June 8, the national average sat at $5.21 a gallon, above $5 in four of the five EIA regions. That is $1.74 higher than the same week in 2025 and $1.55 higher than 2024. The EIA’s own short-term outlook pegs the second-quarter 2026 average at $5.61, the kind of number the industry has not seen since the 2022 spike. Every penny of that hits your account immediately at the pump, in full, before you turn a wheel. None of it waits for the broker to pay you days if not weeks later.

And there is one more weight a lot of operators dragged into this recovery: the high-interest debt they took on just to survive. If you ran a merchant cash advance or maxed credit cards to keep the truck rolling through 2024 and 2025, the monthly cost of servicing that emergency money is eating your margin before it can do anything useful. That is a big reason cash feels tight even with the load board looking the best it has in years.

High Rates Do Not Fix Poor Decisions. Here Is What That Looks Like.

The first version is the operator who runs harder instead of smarter. Rates are up, so he/she chases miles, runs 3,000-mile weeks, takes every load that pays a decent number, and never looks at his deadhead or his fuel economy. He/she is grossing more than they ever have and cannot understand why the account is not growing. One answer is that they are running 18% empty miles, idling six hours a night in comfortable weather, and buying fuel at the most expensive pump on the lane. The hot market is paying them just enough to never notice while ATRI found empty miles industry-wide hit 16.7% during the downturn. Every one of those miles costs you the full variable rate and earns you nothing. You do not outrun that with a bigger rate, you just bury it.

The second version is the operator who confuses gross with profit. He sees a $3,000 load and feels good on the surface. He never calculated that the lane runs him 1,150 miles round trip with a 300-mile deadhead to reposition, which means his real rate per total mile is far below what the settlement says. A high market lets him keep making this mistake because there is enough cushion to absorb it. A normal market does not.

The third version is the one that ends many businesses: the operator who treats a rate recovery as permission to spend. New truck payment, because rates are good. Bigger insurance policy, chrome, a second truck before the first one is dialed in. He is building a higher fixed cost structure on top of a temporary rate environment. When rates normalize, the rate goes back down and the payments do not. He locked in the costs of a good market and will pay them through a bad one.

In every one of these, the rate did not fix the decision. It financed it for a while. The discipline to fix the underlying operation is the only thing that survives a market turn, and the time to do it is now, while the market is giving you margin to work with.

Here is the math that makes it simple. Take a $2,600 load that runs 1,000 loaded miles, and assume you deadheaded 200 miles to get to it. Your gross looks like $2,600. But spread across 1,200 total miles, your real revenue is $2.17 per mile. Now subtract the example ATRI all-in cost, use your ACTUAL all in cost (breakeven) for real calculations. At roughly $2.26 per mile in 2024, and higher now with June diesel at $5.21, you are underwater on that load before you account for the time you spent sitting at the dock. That load felt like a win on the settlement and lost you money in reality. The operator who only reads the $2,600 never sees it. The operator who reads $2.17 per mile against his true cost per mile sees it instantly and books differently.

And the dock is its own silent killer. ATRI calculated that driver detention cost the industry $15.1 billion in 2023, with individual drivers losing 117 to 209 hours a year sitting at shippers waiting on freight that should have been ready. For an owner-operator that is unpaid time, fuel burned idling at $5.21 a gallon, wear on the equipment, and loads you could not take because you were stuck. Detention never shows up on a fuel receipt or an insurance bill. It shows up in your net at the end of the month, and a high rate does nothing to give you those hours back.

The Playbook: Cut Your Variable Costs First

Variable costs move with every mile you turn. They are the fastest to attack and the most within your control on any given day.

Fuel is one of your two biggest costs, so treat it like a strategy, not a stop. With the national average at $5.21 a gallon in June and above $5 in four of five regions, the spread between the cheapest and most expensive fuel on a long lane can run 80 cents to well over a dollar a gallon. Buy on the spread, not on the gauge. Use a fuel-optimization tool or your network’s discount pricing to plan fills in the cheap states and roll past the expensive ones with enough in the tank to make it. On a truck burning 18,000 gallons a year, shaving even 30 cents a gallon through smarter buying is $5,400 straight to your bottom line, no extra miles required. At today’s prices that gap is wider and the savings are bigger than they have been in years.

Slow down and govern the throttle. Every mile per hour over about 62 measurably cuts your fuel economy. Going from 6.5 to 7.0 miles per gallon at $5.21 diesel saves real money on every single mile you run for the life of the truck. This is the cheapest cost cut available and it requires nothing but a lighter foot. The operator doing 75 to feel fast is paying for the privilege out of his own margin.

Kill the excessive idle. Idling burns roughly a gallon an hour producing zero miles. Six hours a night, 300 nights a year, is 1,800 gallons of pure cost. An APU or a bunk heater pays for itself fast at $5-plus diesel, and an idle-shutdown discipline costs nothing at all.

Attack deadhead like it is stealing from you, because it is. Every empty mile costs you the full running cost and earns nothing. Plan backherhauls before you take the front haul. Use partial loads to fill empty space when you are not running a full truck. Cutting your deadhead from 18% to 12% on 100,000 miles a year is 6,000 fewer empty miles, which at your real cost per mile is thousands of dollars you simply stop lighting on fire.

Get serious about preventive maintenance. ATRI’s own data showed that better preventive maintenance directly increases the miles you run between breakdowns, which fell to industry averages around 38,000 miles between unscheduled repairs. A roadside breakdown is the most expensive maintenance there is once you add the tow, the emergency markup, and the lost revenue. Scheduled maintenance on your terms is a fraction of the cost of a failure on the broker’s clock.

The Playbook: Then Restructure Your Fixed Costs

Fixed costs hit every month no matter how many miles you turn, which makes them the quiet killers in a slow week. They are harder to move than variable costs, but the wins are permanent.

Your truck payment is the heaviest fixed cost, so do not let a hot market talk you into a bigger one. Equipment payments hit a record $0.39 per mile and rose 8.3% in a year. If you are shopping for a truck in a strong market, run the payment against your break-even at a normal rate, not the current peak. A payment that works at $2.60 a mile and strangles you at $2.20 is a trap. If you already carry a high-rate note from 2022 or 2023, the improved market may finally let you refinance at a better rate, because your numbers look stronger now than they did then. That is a permanent monthly savings on every mile for the life of the loan.

Shop your insurance every single renewal, and use your safety record as leverage. Insurance is one of the costs that climbed hardest and has not backed off. A clean CSA profile, cameras, and a documented safety record are worth real premium dollars, and the only way to capture that is to make carriers compete for your business at renewal instead of letting the policy auto-renew. This is a fixed cost most operators never negotiate, which is exactly why it keeps climbing.

Consolidate the emergency debt before it eats the recovery. If you are carrying a merchant cash advance at 30 to 40% effective APR or cards at 20%, that debt can swallow the entire raise the market just handed you. Rolling those into a single term loan at a real rate can slash your monthly outflow, and the recovering market has improved your financial profile enough that a consolidation loan that was not available in 2024 may be available now. If you have been operating at least 12 months and can show recovery in recent revenue, that conversation is worth having with a lender who actually works with trucking.

Right-size the fixed overhead you control. Subscriptions, the load board tier you do not use, the parking you are paying for and not using, the dispatch service whose value you have not measured lately. None of these are huge alone. Together they are dead weight on every month, slow or strong, and trimming them is permanent.

Now Close the Cash Flow Gap, Without a Factoring Contract

Once your cost structure is healthy, the timing gap is the last piece, and you can close it without signing with a factoring company if you would rather not.

Quick pay is your closest substitute. Most major brokers offer it: payment in five to seven days instead of 30 to 45, for a fee usually running 2 to 5%. The math is nearly identical to factoring. Three percent on a $2,500 load costs $75 either way. The difference is quick pay is a per-load choice with no contract and no minimum-volume clause. Use it when you need the cash, skip it when you do not.

Tighten your invoicing, which is free. A broker’s net-30 clock starts when they get a clean invoice/POD, not when you deliver. Deliver Monday, photograph and upload the BOL that afternoon, submit a clean invoice by Monday night, and your clock starts Monday. Mail your paperwork Friday or send an invoice with an error that bounces, and you added days to your own wait. Build the habit on every load and you can shave three to five days off your pay timeline across every invoice you cut.

Ask your good brokers for better terms. A broker you have hauled for dispute-free for six months is in a different category than a stranger. The ask is simple: “I have been on time and clean for six months. Can we move to net-15 or set up a quick-pay option?” Some say no but there are many that do in this age. The ones who say yes just improved your cash flow permanently on every future load, at no cost.

Go direct to the shipper when you can. Direct shippers pay the best terms there are, often 15 to 20 days, because you have removed the broker’s payment cycle from on top of theirs. Cutting the broker out improves your rate and your payment speed at the same time. It is the single most powerful move on this list.

The Reserve Is the Thing That Makes All of It Stick

Every move above helps. The reserve is what makes the whole system durable. Get 30 days of operating expenses in the bank, roughly $10,000 to $12,000 for some single-truck operations, and the 35-day payment gap stops being an emergency forever. The reserve covers the wait, the check refills it, and the cycle just runs. It is also what saves you when the tire blows or the truck goes down, the surprise that becomes a crisis for the operator with nothing set aside and a routine Tuesday for the operator who prepared.

You build it a little at a time. Set aside $150 a load, run 20 loads a month, and you add $3,000 a month, reaching a full 30-day cushion in three to four months. The strong market is the time to do it, because the margin to fund a reserve is sitting right there in front of you. The operators who use this market to build that buffer and cut that cost structure are the ones who will read the next downturn as an inconvenience. The ones who use it to outrun their own decisions will read it as the end.

The market turned, and that is genuinely good news. But a better rate is a better number at the end of a 35-day wait, not a cure for a bloated cost per mile and not a substitute for discipline. Fix the costs, close the timing gap, build the reserve, and you turn this recovery into something permanent. Lean on the rate alone and you are just borrowing against the next slow season.

The post When Rates Are Up and Your Cash Is Still Tight. Here Is What Is Actually What Could Be Going On. appeared first on FreightWaves.