The quarterly letter to investors penned by CEO Aaron Graft for the first quarter sets new metrics for the trucking-focused financial services company, as well as praising the group’s factoring division.

The letter, and Triumph Financial’s (NASDAQ: TFIN) first quarter earnings, were released Tuesday after the market close. The company’s earnings call is Wednesday.

Graft’s letter, several pages of detail that is unique in the industry, has in the past been more likely to focus on Triumph Financial’s Payments segment than Factoring, which is a long-held business. Payments, with its open-loop auditing and payment network, is the more disruptive offering at Triumph Financial and is targeted to be an increasing percentage of the company’s profitability.

But the most praise from Graft this quarter was targeted at Factoring, though results in Payments were strong as well.

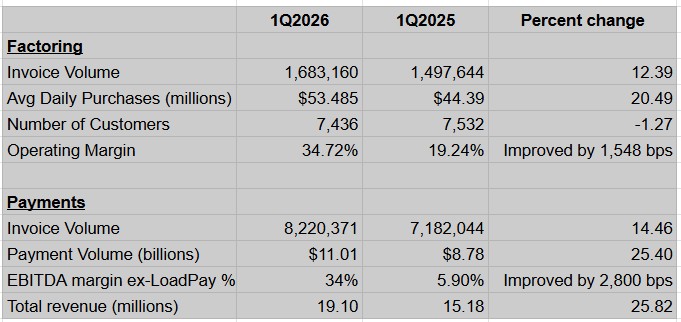

Graft’s praise for Factoring came in the fact that it increased its total purchased volume of invoices by 20.5% from a year ago, and 4.6% increase sequentially, even though the first quarter tends to be soft. “That is robust growth for a mature business,” Graft said. “I am also impressed with how our team outperformed seasonality in the first quarter.”

Factoring invoice volumes declined 3.5% while Payments dropped 9.2%, another point of praise from Graft for the Factoring segment relative to its corporate peer.

In discussing the new metrics, which Graft described as Triumph Financial’s “North Star,” the CEO said they are the numbers “that matter most.”

The new benchmarks are total revenue growth in Transportation, which includes both Factoring and Payments but not banking; the operating margin in Factoring; and the EBITDA margin in the Payments segment, excluding the relatively new LoadPay product, a wallet-like offering that is targeted directly at the finances of individual drivers.

It also includes the gross margin for the company’s relatively new Intelligence unit, which based on past performance is projected to have annual recurring revenue of $8.4 million.

Still looking at growth, but focus on new KPIs

“We used to talk about logos, density, and product roadmap; we now talk about revenue growth and margin,” Graft said of the new North Star goals. “This does not mean we have stopped innovating or pursuing growth — it means we expect those efforts to show up in our numbers. We will continue putting forth the KPIs that we believe are the best signal of achieving long-term value creation. Investors will be able to judge both the merit of our recommended KPIs and our performance against them.”

As for those goals in the quarter, transportation revenue growth compared to the first quarter of 2025 was up 23.5%; the long-term target is greater than 15%.

Less than target but well above last year

Factoring’s long-term operating margin target is more than 40%; it was 34.7% in the quarter. The Payments EBITDA margin target, excluding LoadPay, is greater than 50%; for the first quarter, it came in at 34%. A year ago it was less than 6%.

That 40% target for Factoring, Graft said, “is rare air in commercial finance. To consistently achieve that margin usually requires proprietary data embedded distribution and network effects.”

Graft noted that the Factoring segment does have “add-on” services, including its Factoring as a Service offering, LoadPay and the Intelligence segment.

In the letter’s first mention of AI, Graft said personnel numbers are declining in the Factoring segment and attributed part of that to AI.

The Graft letter said the volume of invoices processed in Factoring for the first quarter of 2025 was 1.498 million, with 266 employees in the segment. Factoring volume of 1.683 million invoices in the first quarter of 2026 and was handled by 235 employees.

“While several initiatives remain in progress, early results are translating into improved throughput and workflow efficiency, supporting continued increases in invoices processed per employee,” Graft said in his letter. “These efforts are strengthening the scalability of our operating model, enabling us to support growth without proportional cost expansion, with the benefits reflected in our expense outlook.”

In discussing the performance of Payments, Graft noted that repricing of existing contracts was “the largest growth driver in the quarter, but we also brought on and ramped up several new relationships while deepening relationships with others throughout cross-selling efforts.”

The Graft letter also noted that Payments customers generally are charged on a per invoice basis, not as a function of the size of the invoice as is done in Factoring. “So invoice counts are a better gauge of revenue growth than Payments volumes,” he said. Invoice volume in Payments was up about 14.5% year-on-year.

More articles by John Kingston

After CBS report, C.H. Robinson seeks to deflect safety responsibility to FMCSA

California regulators have started a regulatory push on diesel TRU emissions

ATBS: average truck driver earnings in 2025 held mostly stable from ‘24

The post Triumph Financial sets new metrics, has strong quarter in factoring appeared first on FreightWaves.