Alain Bedard, the CEO of TFI International, has never been shy about discussing the problems of his U.S. LTL operations, which the company built from the acquisition of UPS Freight in 2021.

On a previous earnings call with analysts, he said the U.S. LTL operations of TFI were“too fat.” On another call, he called some of the group’s practices “stupid.”

Bedard had been more positive about the sector’s prospects in some recent calls. But on Monday’s call with analysts after the company’s challenging earnings were disclosed, even alongside an optimistic outlook, Bedard once again brought up the woes of TFI’s U.S. LTL sector which he believes have not been fully conquered.

HIs statements came against a backdrop of a change in TFI’s earnings disclosures that no longer can be used to contrast the performance of U.S. LTL at TFI with Canadian LTL. The financial reports of the two have been merged into one, which might bring a sigh of relief to the U.S. team since the numbers were never favorable compared to their counterparts in the Great North.

The combined adjusted operating ratio for North American LTL at TFI deteriorated to 95.3% from 93.1% from the first quarter of 2025, but it is no longer possible to look at that number and know the relative direction of the Canadian and U.S. operations.

Praise for the management team

Even as he discussed some of the lingering problems at U.S. LTL, Bedard was complimentary on Monday’s call of the people running those operations.

“We’re still in a position of working hard to get closer to the service level of our peers,” Bedard said.

He later said the U.S. LTL operations at TFI (NYSE: TFII) has “stability on the commercial side” and “we have a lot of good stuff going on with our team. They are all pumped up after three years of a very difficult environment for us.”

But Bedard’s review of its operations suggested it had underlying issues that still are going to need a lot of work to fix.

“Our service is slowly again improving,” he said. “Customers are starting to see us in maybe a different way. These guys are finally getting their act together. We’re far from perfect but we are improving.”

As an LTL carrier, Bedard said, “the worst thing that you can have is to try to sell a service, and the service is not there.”

An LTL carrier is “supposed to pick up the freight, and then we don’t show up. That’s not too good, right? So that is what the operating guys have been working on.”

He also cited reducing the company’s claims percentage further. (The cargo claims percentage of 0.6% in the first quarter was flat to a year ago.)

Issues with its previous owner

Where Bedard was most critical was in what could be seen as a broadside against the way UPS ran its LTL operations. “The culture is the culture of the old days of laissez faire, and I don’t really care,” Bedard said. “You’re going to say, Alain, you bought the company five years ago.”

Bedard said the earlier culture was that of a “monopoly.” He also said the U.S. LTL operations of TFI are now a “discounted carrier compared to some of my peers, and the reason is because our service is not where it should be.”

He revived earlier criticisms that the density in the U.S. operations is a burden. “We’e saying to our commercial guys, don’t give me a customer where I have to run 70 miles to pick up the shipping,” he said. “This is not what I want. I want something that is closer to my terminal, to improve my density. I want more shipments per stop to improve my cost per shipment.”

But even as old criticisms were raised, Bedard and CFO David Saperstein were optimistic about the freight market, despite a quarterly earnings report that on its surface showed little year-on-year improvement.

Wall Street fans of the company

For all the discussions of a tough market, TFI stock has been on a roll. It’s up about 73.3% in the last 52 weeks and 32.1% in the last month.

The earnings report was good enough to result in the transportation research team at Bank of America (BOA) led by Ken Hoexter upgrading its rating on TFI to Buy from Neutral after the earnings release.

TFI, in its earnings report, estimated second quarter EPS of $1.50 to $1.60 per share with Bedard saying he wouldn’t go further out than that because of uncertainty regarding Mexico/U.S./Canada trade. The BOA report said its estimate had been $1.28 and Wall Street consensus was $1.31.

“We see potential for strong cash generation, idiosyncratic U.S. LTL operational improvement, and upside from supportive specialty/flatbed rate dynamics,” BOA said in its analysis.

In response to an analyst’s question about the company’s Truckload segment, which has revenue that is slightly less than the combined LTL operations, Bedard said conditions have started to improve. “Our customers are now asking, hey, can you help me?” Bedard said. “They are saying, can we be partners? Because it’s always the same story when the markets start to tighten up, shippers want to be partners with truckers.”

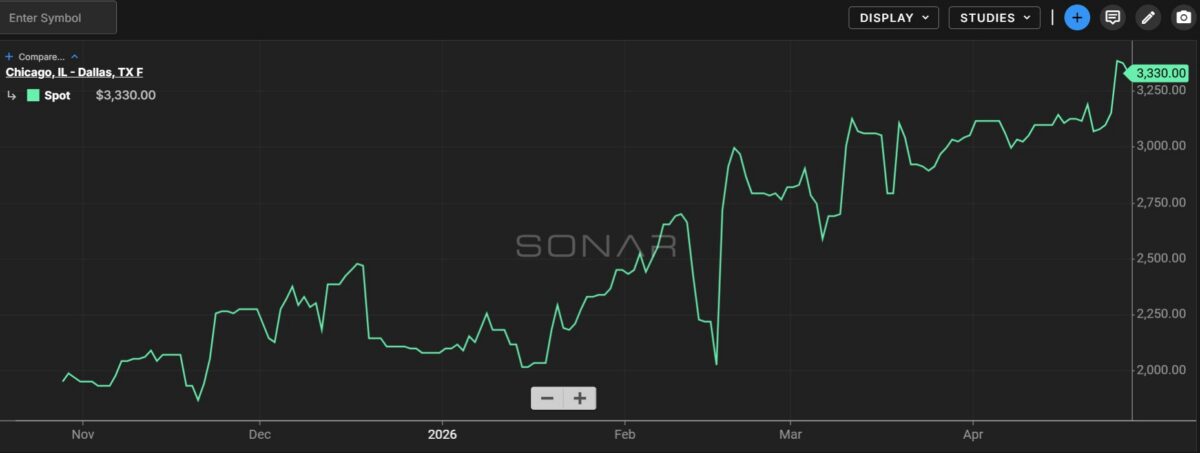

The rip-roaring flatbed market led to analyst questions about how TFI was benefiting. Bedard said the company’s specialty truckload operations, which includes the legacy Daseke business, has been strengthening alongside the rising flatbed market rates.

Spot Chicago to Dallas flatbed rates, per SONAR

TFI announced the purchase of flatbed operator Daseke in late 2023. Bedard also had been open in the past about its struggles.

But on the first quarter earnings call, Bedard said investments in such areas as technology and financial systems in the legacy Daseke business means that “we’re starting to see a little bit of light at the end of the tunnel in terms of demand. So I feel really good about where we’re at now.”

“Our revenue per mile is up and we drive more miles per truck per week,” he said. Productivity also is improved, Bedard said, as the team does “more with less” as it has cut the size of its fleet. TFI’s truckload fleet is down 8.4% from a year ago.

On LTL, both Bedard and Saperstein said the first quarter numbers were impacted more than usual by winter weather in January and February. But March was strong, they said, and April continued the trend, each of them up about 8% in volume year-over-year.

The U.S. LTL operations, Bedard said, have not experienced organic growth in a “long time.” But the group’s second quarter performance is likely to at least be flat to the prior year. That is an improvement as several key indicators on TFI’s LTL operations were all negative year-over-year, including revenue before fuel and revenue per hundredweight.

“I think we’re going to finally turn the page on a very difficult ‘23, ‘24 and ‘25, ‘25 being the worst of the three,” Bedard said. “I think that ‘26 is going to be a transition year to a much better future for us in the quarters to come.”

More articles by John Kingston

FMCSA issues mandatory non-domiciled CDL directives

Why truckers should care about DOL’s latest proposal on joint employers

Triumph Financial sets new metrics, has strong quarter in factoring

The post TFI’s Bedard optimistic about U.S. LTL, but some of its issues persist appeared first on FreightWaves.