The April installment of the State of Freight webinar, hosted by FreightWaves CEO Craig Fuller and Head of Freight Market Intelligence Zach Strickland, pointed to a freight market that remains structurally tight—even as seasonal softness and macro uncertainty cloud near-term visibility.

From geopolitical disruptions in the Middle East to upcoming enforcement events and summer demand patterns, the discussion highlighted a market transitioning from recovery into a more durable tightening cycle. Here are five key takeaways:

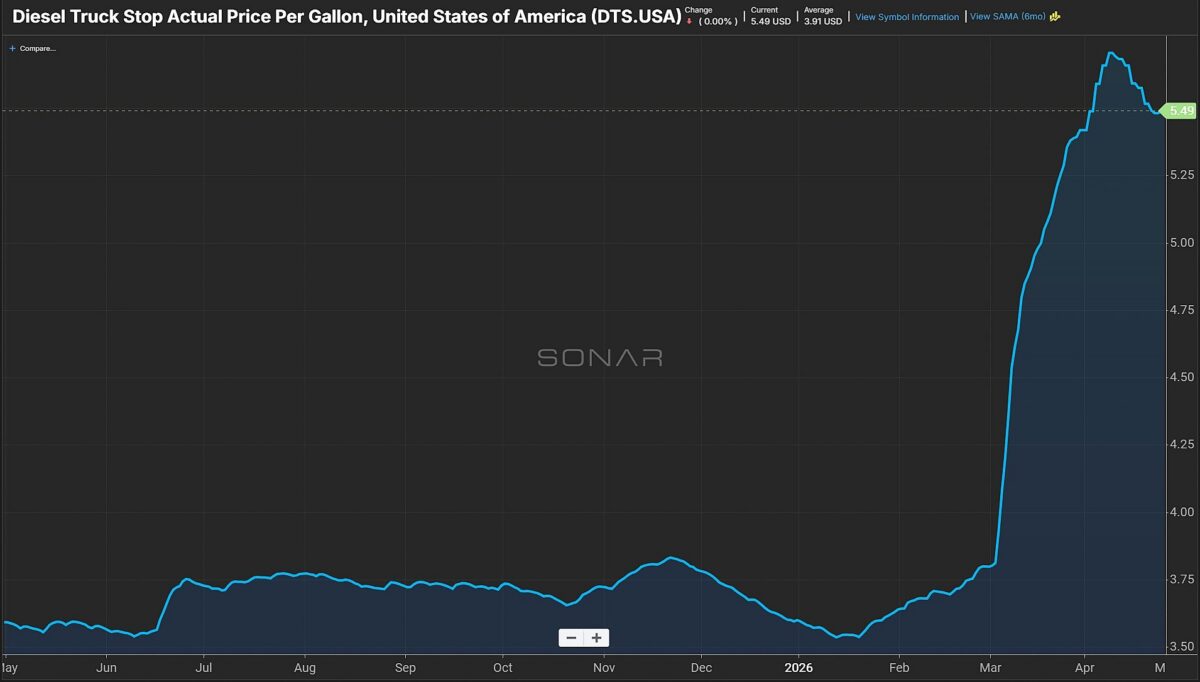

Iran conflict driving fuel volatility, but not derailing demand

Fuller said the ongoing conflict in Iran is having a clear impact on fuel markets, though the broader freight economy remains resilient.

“All of it is tied to Iran… high oil prices are a factor at Iran… but there’s nothing in any of the data that says that higher fuel costs… is sapping the U.S. economy,” Fuller said

Strickland noted that diesel volatility has been reactive to geopolitical developments, especially around the Strait of Hormuz.

“We saw this pretty significant spike in retail diesel… and then as we started to see the end of the military conflict… the price of diesel came down,” Strickland said.

Fuller, emphasizing that fuel costs alone are not dictating freight pricing power, said the “tightness in capacity enables motor carriers to have pricing power… not necessarily diesel.”

Strickland added that carriers are still recovering fuel costs through rates in a tightening environment. “If you look at what the rates are… you’ve been able to recover all of that and potentially more,” he said

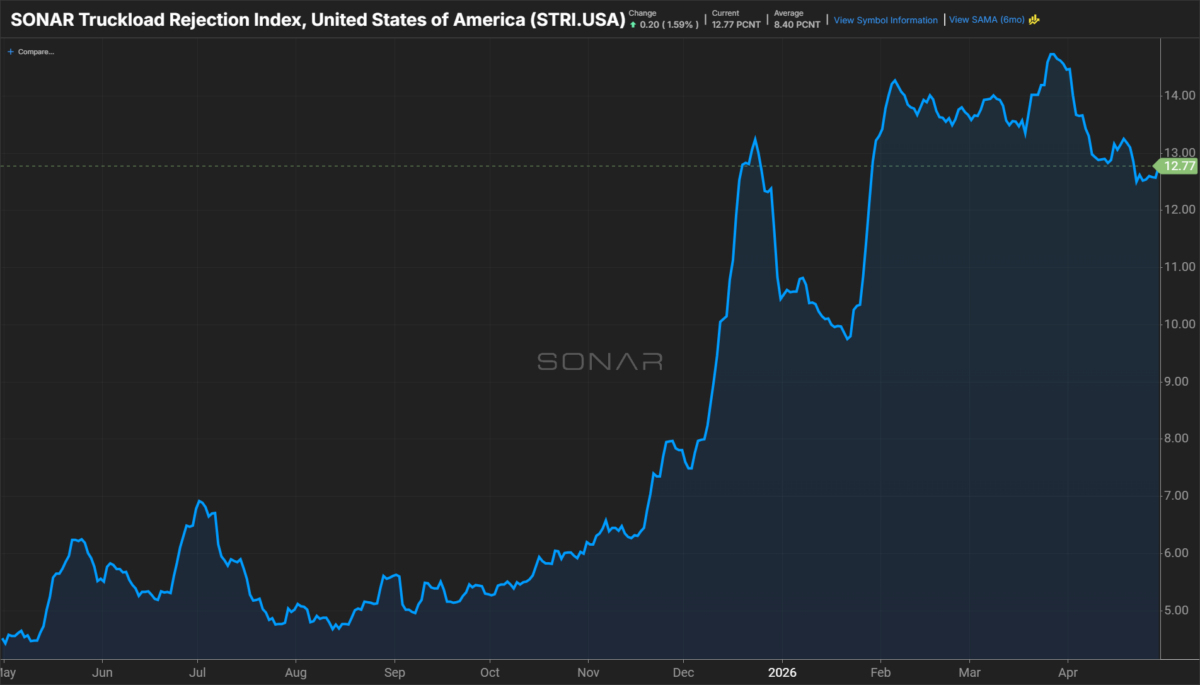

April: inflection point or seasonal “speed bump”?

Both executives pushed back on the idea that April’s softer trends signal a reversal.

“April has been… just kind of a sideline,” Strickland said. “It’s not up and to the right the way we saw it in March.”

Fuller countered that the market remains far stronger than year-ago levels.

“We’re talking about rejection rates… at 12.7%… these are levels that we haven’t seen in years,” Fuller said.

He also pointed to stronger macro signals underpinning freight. “You’re starting to see broader economic data… indicating much stronger activity than most people expected.”

Strickland framed April as a typical seasonal trough rather than a turning point.

“April is historically a weak month… you end up in May with a massive acceleration,” Strickland said.

Roadcheck could tighten already constrained capacity

Looking ahead, both warned that the upcoming CVSA International Roadcheck could meaningfully disrupt capacity.

“We’re going to see capacity come off the roads… more than usual,” Fuller said.

He added that stricter enforcement and compliance scrutiny are already influencing driver behavior.

“Drivers know that the DOT is getting directives to really crack down… so I think we’re going to see more capacity taken off the road,” Fuller said.

Strickland said the impact could be amplified by an already tight market, adding “there is very little excess capacity… so the market is much more sensitive.”

Fuller expects rejection rates to spike during the enforcement period.

“We will get into the 16%–17% range for a week,” he said.

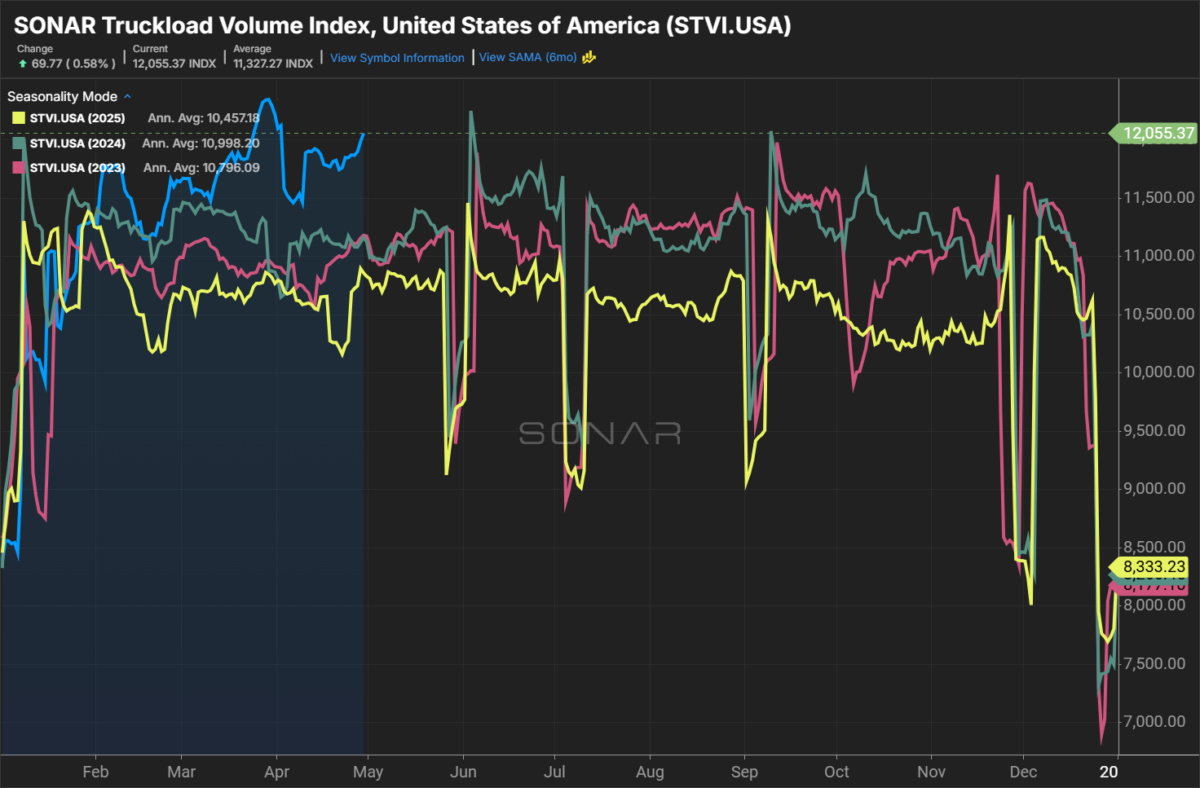

Summer demand signals point to stronger freight cycle

Both executives highlighted strong indicators heading into peak summer shipping.

“Demand has gotten stronger… and we’re seasonally about to go into a much stronger demand cycle,” Strickland said.

Fuller pointed to structural drivers beyond traditional retail.

“June is the biggest month of the year… you have produce, construction, industrial production—all coming together,” Fuller said.

He also emphasized that industrial activity—not consumer retail—is driving the current cycle. “What’s been driving this market is not consumer retail… it is largely industrial,” Fuller said.

Strickland added that volumes are already showing strength — “volumes are up 11% year over year… probably 12% to 13% now.”

Risks and opportunities shaping the road ahead

The webinar closed with a look at structural shifts that could reshape the freight market.

Fuller pointed to regulatory and legal risks, including broker liability and compliance crackdowns.

“This is going to be probably the biggest story of the summer… it will completely change the way brokers operate,” Fuller said.

He also highlighted capacity constraints tied to regulation, adding “you’re talking about the net impact… as much as 600,000 to 800,000 drivers.”

Strickland noted that rate pressure is already building.

“We’re already at about a 10% increase… and we’re going to see that grow throughout the year,” Strickland said.

Fuller said the market has clearly moved past the downturn.

“There is no freight recession right now… we are clearly done with it,” he said.

The post State of Freight: Freight recession ‘over’ as demand builds into summer appeared first on FreightWaves.