After $2 billion in network investments, less-than-truckload carrier Saia is expecting to soon see a payoff as cost and operational enhancements are converging with better demand. The company is also seeing more freight opportunities now that it runs a national network.

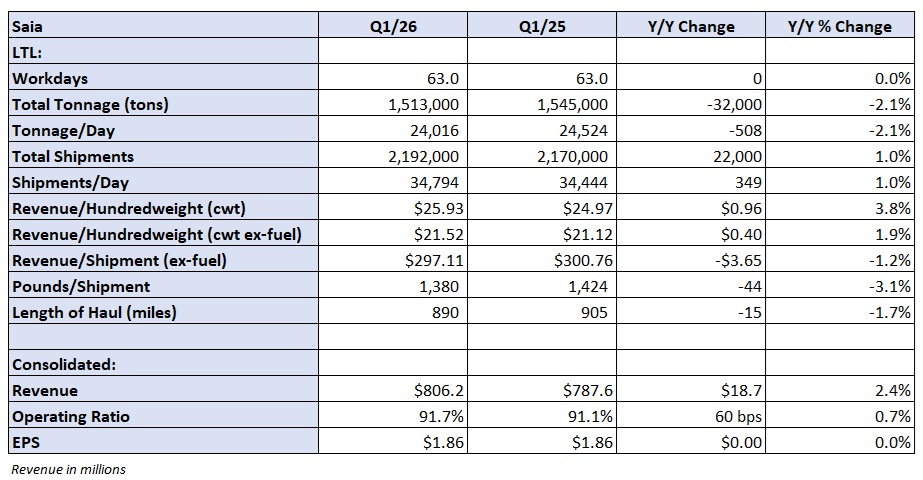

Saia (NASDAQ: SAIA) reported first-quarter earnings per share of $1.86 on Thursday before the market opened. The result was flat year over year and 4 cents ahead of the consensus estimate. A lower tax rate was a 2-cent tailwind.

Revenue increased 2% y/y to $806 million, which was $18 million better than analysts’ expectations. Executives said on a quarterly call that customers are “getting more positive” and that many of its legacy service centers are again seeing growth given the optionality a national footprint provides.

Tonnage fell 2% y/y in the quarter as a 1% increase in shipments was offset by a 3% decline in weight per shipment. Revenue per hundredweight (yield) increased 4% (2% higher excluding fuel surcharges). The lower average shipment weight was a tailwind to the yield metric.

The first quarter contended with a tough prior-year tonnage comp (plus-12.8%). On a y/y comparison, tonnage fell by 7% in January and 2.7% in February. Tonnage was up 2.8% in March. Management said volume improvement in late-March helped offset some of the weather disruptions in January and February. Saia’s terminal network has a high concentration across the South, which was significantly impacted by the storms.

The March strength continued into April as tonnage increased 6.5% y/y. The prior-year comps eased in April (plus-4.4%) and turn negative in May. Weight per shipment improved throughout the quarter.

Contractual renewals averaged 6.7% in the quarter (up 12.8% on a two-year-stacked comp). Revenue per shipment (excluding fuel) was down 1% y/y, but improved sequentially through the quarter.

Q2 guide implies 87.5% OR

The company reported a 91.7% first-quarter operating ratio (inverse of operating margin), which was 60 basis points worse y/y and 40 bps worse than the adjusted fourth-quarter OR of 91.3% (excludes a one-time insurance item). The company previously said it hoped to outperform normal sequential OR deterioration of 30 to 50 bps.

The spread in cost per shipment and revenue per shipment was negative by 130 bps in the quarter. However, that was much smaller than the 560-bp negative spread booked in the fourth quarter.

Salaries, wages and benefits expenses (as a percentage of revenue) were 60 bps lower y/y even as health insurance costs and workers’ comp claims moved higher. Improved productivity (shipment touches down 2.5%) allowed for a 6.3% y/y reduction in headcount (7.9% lower excluding linehaul drivers). Salaries and wages costs moved 1.8% lower y/y due to the productivity improvements.

Depreciation and amortization expenses were 20 bps higher y/y given previous terminal and equipment additions. The company’s roughly 40 new facilities are operating at upper-90s ORs.

Saia normally sees 250 to 300 bps of sequential margin improvement in the second quarter. However, it’s calling for 400 to 450 bps of improvement this year (assuming normal seasonal demand trends). Firming volumes and a lower starting point are behind the outlook. The guide implies an 87.5% OR at the midpoint, which would be slightly better y/y.

A full-year net capex range of $350 million to $400 million was reiterated. Net capex was $544 million in 2025 and $1.05 billion in 2024.

Shares of SAIA were up 5.7% at noon EDT on Thursday compared to the S&P 500, which was up 0.5%. The stock is up over 30% year-to-date.

More FreightWaves articles by Todd Maiden:

- Old Dominion eyeing y/y margin improvement in Q2

- Landstar says April yields ‘significantly’ outpacing seasonality

- ArcBest seeing positive trends amid market inflection

The post Saia eyes margin turnaround amid improving demand appeared first on FreightWaves.