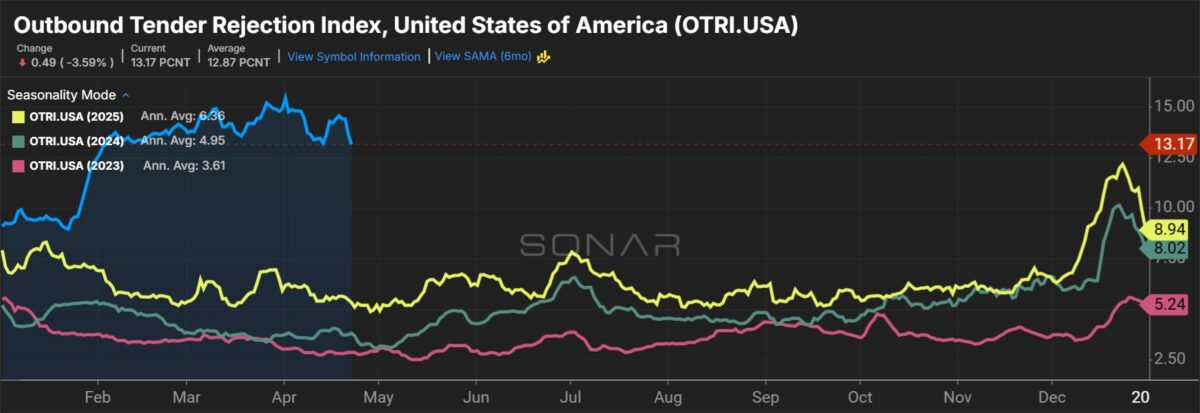

Knight-Swift Transportation anticipates significant contractual rate hikes during the current and upcoming bid cycles as the freight market emerges from a nearly four-year downturn. Strict regulatory enforcement and the recent fuel price shock are driving non-compliant and underperforming operators out of the market. Even without a notable pickup in demand, supply constraints have been severe enough to force shippers to contemplate realignment with asset-based carriers providing meaningful scale.

The Phoenix-based company’s CEO, Adam Miller, told analysts on a Wednesday quarterly call that mini-bid activity is increasing as shipper routing guides fail. He said some carriers are no longer honoring rates negotiated just one or two months ago and that some of its customers are already looking to lock up peak-season capacity. After capturing mid-single-digit contractual rate increases in its truckload business to start the year, the company is now eyeing high-single- to low-double-digit increases on the remaining 70% of its book.

“I don’t think we’ve ever really seen the pressure on capacity … coming from regulatory forces versus just normal economics,” Miller said. “I think we could see more capacity coming out of the network than we typically would see in a cycle, and I feel like that could be a catalyst to really drive a strong bid season this year [and] also into next year.”

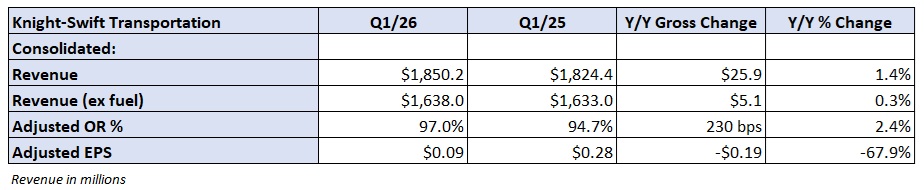

Knight-Swift (NYSE: KNX) reported a headline net loss of $1.3 million, or 1 cent per share, for the first quarter. Adjusted earnings per share of 9 cents were in line with the negative earnings revision the company provided last week. Analysts were expecting adjusted EPS of 25 cents heading into earnings season.

Adjusted EPS included several nonrecurring items. Headwinds included: 8 cents per share from a negative less-than-truckload claim development, 5 to 6 cents per share from weather and fuel headwinds, and 2 cents per share from an adverse value-added-tax ruling in its Mexico business. A roughly $8 million decline in net interest expense largely offset a similar decline in gains on equipment sales during the period.

The company reiterated its second-quarter adjusted EPS guidance range of 45 to 49 cents, which it had also provided last week.

U.S. Xpress fleet appears to be right-sized

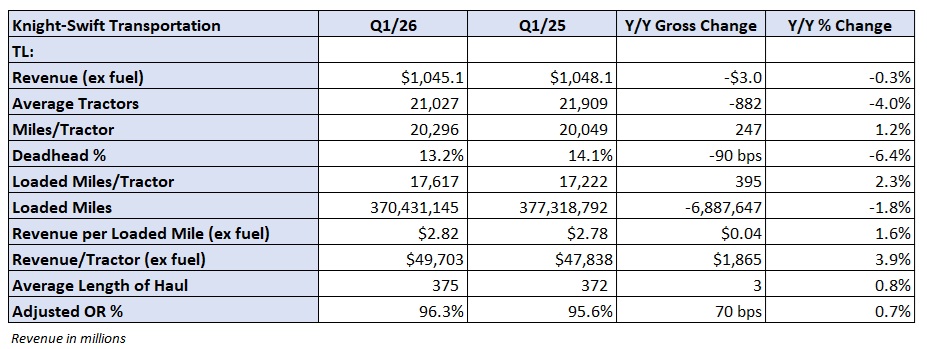

Truckload revenue was flat y/y at $1.05 billion, excluding fuel surcharges. A 4% increase in revenue per tractor offset a 4% decline in average tractors in service. The company has culled the fleet count over the past several quarters to improve asset utilization. Loaded miles per tractor improved 2.3% in the period, with revenue per loaded mile (excluding fuel) increasing 1.6%.

The segment booked a 96.3% adjusted operating ratio (inverse of operating margin), which was 70 basis points worse y/y. Inclement weather and surging fuel costs were among the headwinds.

The bulk of the tractor drawdown occurred at the U.S. Xpress fleet, which Knight-Swift acquired in 2023. Total annual revenue at U.S. Xpress is roughly $1.7 billion currently, down from $2.2 billion in 2022, which had the benefit of the tail-end of the upcycle. The actions were taken to improve freight mix and margins. U.S. Xpress is closing the gap to the legacy Knight and Swift fleets, operating at a margin that lagged by 300 bps in the quarter.

The TL unit typically operates at a mid-80s OR in a normal market. Roughly 70% of its assets are currently operating in one-way and over-the-road configurations, which Miller said are the most levered to an upcycle. True spot exposure in the business has increased a couple of percentage points to a low- to mid-teens range. The midpoint of management’s second-quarter guidance implies a 93.1% adjusted OR.

LTL could get back to double-digit margins by year-end

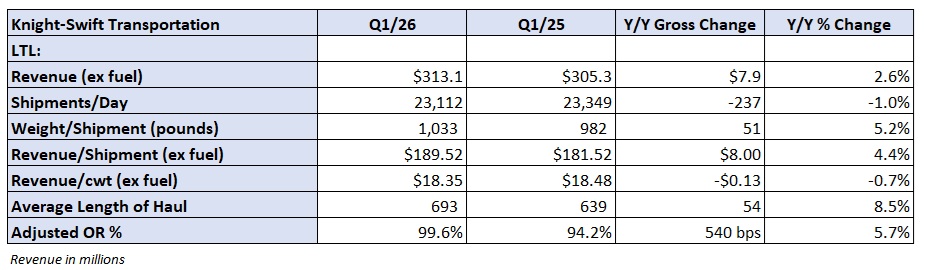

Costs associated with acquisition integrations and rapid organic terminal growth have weighed on LTL margins. The segment reported a 99.6% adjusted OR in the quarter, which was 540 bps worse y/y. However, the adverse claim development was a 570-bp headwind. Guidance calls for a low-90s OR in the second quarter, with the potential for sub-90% later this year.

The freight mix is improving. Weight per shipment was up 5% y/y to the highest level since 2021, when Knight-Swift entered the business. Also, variable wage per shipment (notably dock wages) and other variable costs are declining, and the aforementioned growth-oriented expenses are largely in the rearview. However, Knight-Swift still needs to acquire a Northeast carrier to complete its national terminal network.

Revenue increased 3% y/y to $313 million as a 1% decline in daily shipments was more than offset by a 4% increase in revenue per shipment (excluding fuel). Tonnage accelerated throughout the quarter—up 1.6% y/y in January, up 2.6% in February and 6.9% higher in March. Management said rate renewals continue to increase by a mid-single-digit percentage.

Other Q1 takeaways

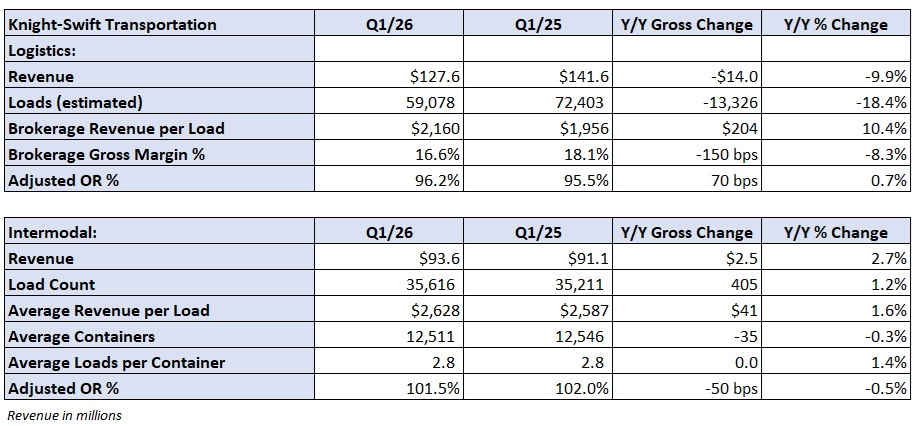

Brokerage load count was down 19% y/y as the company continued to screen against non-compliant carriers and mitigate cargo theft risks across the platform. A 10% increase in revenue per load helped limit the segment’s revenue decline to 10%. A 96.2% adjusted OR was 70 bps worse y/y as a spike in purchased transportation costs compressed gross margin by 150 bps to 16.6%.

The company expects improving brokerage results as it reprices its contractual book of business throughout bid season.

The intermodal unit booked another operating loss. A 101.5% adjusted OR was 140 bps worse sequentially but 50 bps better y/y. Revenue increased 3% as load count and revenue per load “improved progressively throughout the quarter.”

Intermodal load count is expected to be up y/y by a high-single- to low-double-digit percentage in the second quarter, with the unit likely seeing breakeven or better operating results (OR to improve 150 to 250 bps sequentially).

All other segments, which include revenue from support services to third parties, combined for a $7.1 million operating loss in the quarter. A change in accounts receivable financing was a $5.2-million headwind. The unit also had startup costs from new warehousing contracts, and some warehousing project activity was pushed into the second and third quarters.

All other segments are forecast to generate $14 million to $18 million in adjusted operating income in the second quarter.

More FreightWaves articles by Todd Maiden:

- Werner doubling intermodal fleet in Mexico

- Knight-Swift cuts Q1 guide; remains upbeat on TL fundamentals

- J.B. Hunt says TL inflection ‘structural,’ not temporary

The post Knight-Swift says shippers already seeking peak-season capacity appeared first on FreightWaves.