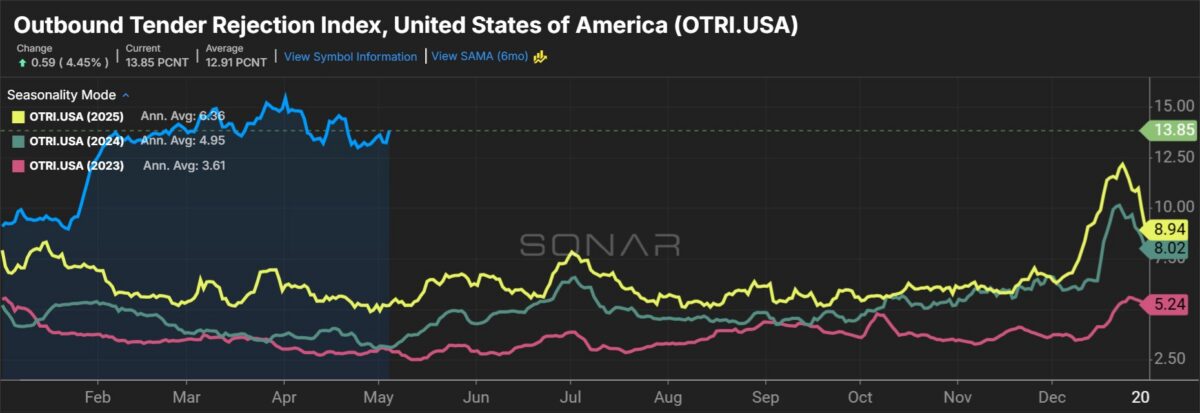

Supply chain managers reported a very tight freight market during April, noting extreme declines in capacity with corresponding surges in transportation rates.

The Logistics Managers’ Index—a diffusion index in which a reading above 50 indicates expansion, while one below 50 signals contraction—returned a 28.4 reading for transportation capacity in April. That was 10.9 percentage points lower than the March reading and the second-fastest rate of decline captured by the dataset in its nearly 10-year history. (The highest rate of decline was recorded in September 2020 at “the kick-off of the first pandemic peak season.”)

Transportation prices (95) were up 5.6 points in the month. April marked the second-fastest growth rate for pricing. At a spread of 67 points, the two indexes have never been further apart.

“Taken together, this means that we have never before tracked the transportation metric getting simultaneously tighter or more expensive,” the Tuesday report said. “Freight markets were already on a strong upward trajectory coming into 2026, the closure of the Strait of Hormuz and subsequent increase in fuel costs have supercharged these movements.”

While “the capacity crunch is being felt everywhere,” it is more pronounced at large companies (over 1,000 employees) and at upstream firms (manufacturers and wholesalers). “These differences likely reflect the stock up happening at manufacturers and wholesalers as they attempt to compensate for increased fuel prices through freight consolidation,” the report said.

Transportation utilization (69.6) increased 6.7 points to the highest reading since November 2021. Upstream companies returned a 76.1 reading, which was 21 points higher than downstream retailers.

Logistics managers surveyed expect the transportation market to remain very tight over the next 12 months, returning future readings of 33.2 for capacity, 74.5 for utilization and 93.9 for pricing.

All-in logistics costs surge again

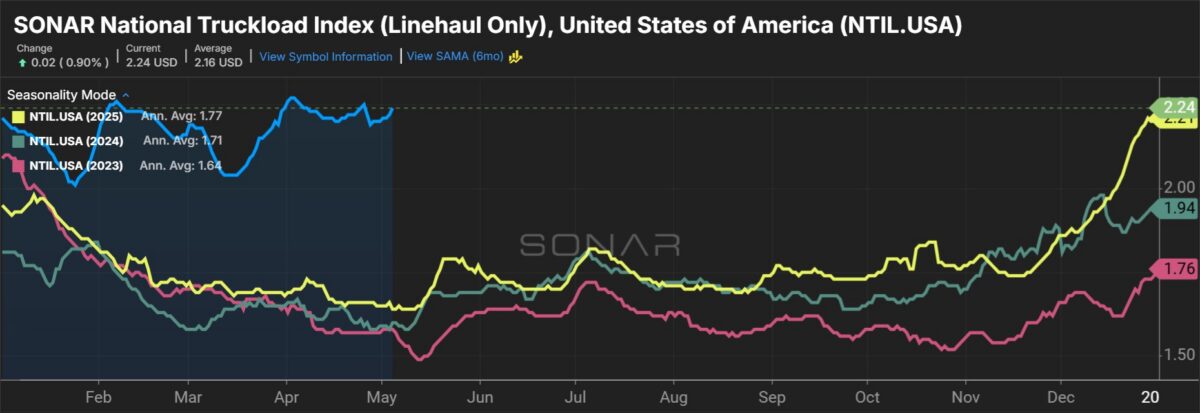

The overall LMI stood at 69.9 in April, up 4.2 points sequentially and the highest reading since April 2022. The “continued expansion in the freight market” drove the change.

Inventory levels (56.3) increased 1.5 points, with most of the build occurring in the back-half of the month. Inventory costs (74.7) dipped 1.5 points in the month, but continued “to increase at a rapid pace.” Costs were 7 points higher for small firms, “which may have less flexibility with moving orders around and consolidating shipments due to their lower economies of scale.”

The warehousing market tightened again.

Warehouse capacity (45.5) contracted as utilization (64.4) expanded 4.6 points, pushing warehouse prices (72.7) up 5.3 points and into “significant expansion” territory. These metrics also showed tighter conditions at the upper levels of the supply chain.

Aggregate logistics costs (inventory, warehousing and transportation) stood at 242.4, the fastest rate of expansion since April 2022.

“Supply-driven inflation is more difficult for the Fed to combat that demand-driven inflation because higher interest rates cannot create greater supply (in some cases they actually may hinder supply),” the report cautioned. “If logistics costs remain elevated, it is likely there will be at least some inflation.”

The LMI is a collaboration among Arizona State University, Colorado State University, Florida Atlantic University, Rutgers University and the University of Nevada, Reno, conducted in conjunction with the Council of Supply Chain Management Professionals.

More FreightWaves articles by Todd Maiden:

- Losses continue at TL carrier Pamt Corp.

- Schneider targeting significant rate recovery in bid season

- XPO could soon see sub-80% ORs

The post Freight capacity plummets, prices skyrocket in April appeared first on FreightWaves.