Although several year-on-year operating comparisons for TFI International (NYSE: TFII) were negative compared to the first quarter a year ago, the company in its prepared statement released in conjunction with the earnings was upbeat.

The bottom line numbers were positive for TFI in one sense. According to SeekingAlpha, the company’s non-GAAP earnings per share of 69 cents per share beat consensus forecasts by 8 cts. Revenue of $1.95 billion was better than consensus by $50 million.

““We easily exceeded our first quarter earnings outlook on stronger revenue and higher profitability for both Truckload and Logistics despite adverse weather early in the quarter, thanks to the hard work of our talented team and benefitting from our strategic investments in recent years,” Alain Bédard, chairman, president and CEO said in the statement.

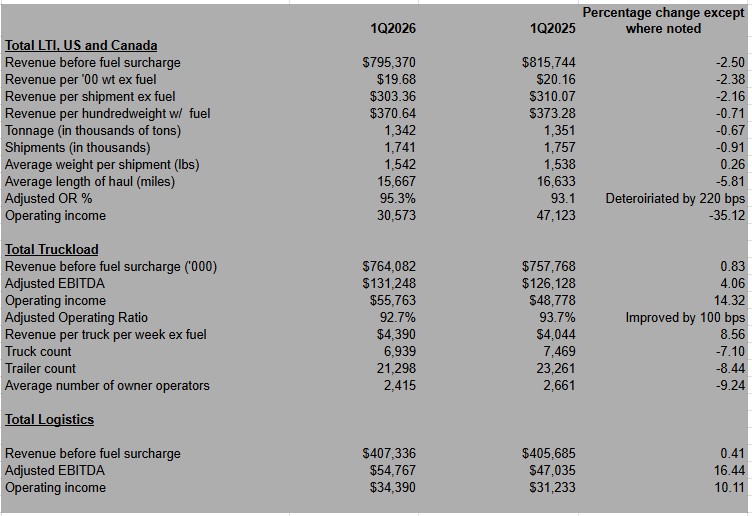

The first quarter was the introduction of a revised system for reporting LTL earnings at TFI. Previously, the company broke out separate performance figures for its U.S. and Canadian LTL operations. But that has ended, so all LTL figures are for the company as a whole.

LTL continued to struggle by some measurements. The combined operating ratio (OR) rose 220 basis points to 95.3%. Operating income declined 35.12% and its revenue per shipments excluding fuel, which is known as yield in the LTL sector, dropped 2.16% to $303.36. Adjusted EBITDA was down 14.4% to $79.2 million.

The Truckload sector fared better. Total revenue inched up 0.83%, adjusted EBITDA was up just over 4%, and operating income rose 14.32%.

TFI’s revenue split between LTL and Truckload was 51% for LTL and 49% for Truckload.

Adjusted EBITDA in TFI’s Logistics segment rose 16.44%.

“Combined with our team’s sharp focus on efficiencies and bottom-line profitability, TFI is well positioned as freight dynamics build on the improvement in March,” Bedard said in the statement. “All the while, we continue to fortify our balance sheet with ample free cash flow that facilitates our timely and strategic allocation of capital as well as our attractive dividend, with the return of excess capital a cornerstone of our mission to produce long-term shareholder value.”

Even in its toughest quarters, TFI management has always touted the company’s cash flow. But net cash flow in the quarter from operating activities dropped to $121.5 million from $193.6 million. That was also a big drop from the fourth quarter, when TFI reported net cash flow from operating activities of $282.2 million.

TFI’s presentation blamed the decline in that figure on an increase in accounts receivable relative to accounts payable, which have different payment periods for fuel and payroll.

TFI gave a strong estimate on second quarter earnings, saying it expects second quarter 2026 adjusted diluted EPS to be in the range of $1.50 to $1.60. That is compared to 69 cents in the first quarter. On the company’s earnings call, CFO David Saperstein said March was far better than the first two months of the first quarter and said April had been stronger still.

More articles by John Kingston

FMCSA issues mandatory non-domiciled CDL directives

Why truckers should care about DOL’s latest proposal on joint employers

Triumph Financial sets new metrics, has strong quarter in factoring

The post First look: TFI’s LTL group struggled, Truckload shows improvement appeared first on FreightWaves.