The benchmark price used for most fuel surcharges has fallen for the 12th time in 13 weeks in an oil market that remains bifurcated to an almost historical level.

The Department of Energy/Energy Information Administration average weekly retail diesel price declined 9 cents/gallon to $4.578/g, effective Monday and published Tuesday. That price decline in those 13 weeks would have been consecutive except for a one-week big jump in early May.

Prices on the street appear to be volatile enough that three indicators of their number are producing a significant disparity. The AAA average retail diesel price for Tuesday was $4.765/g, up a little less than one cent from the prior day in the first increase recorded in almost a month.

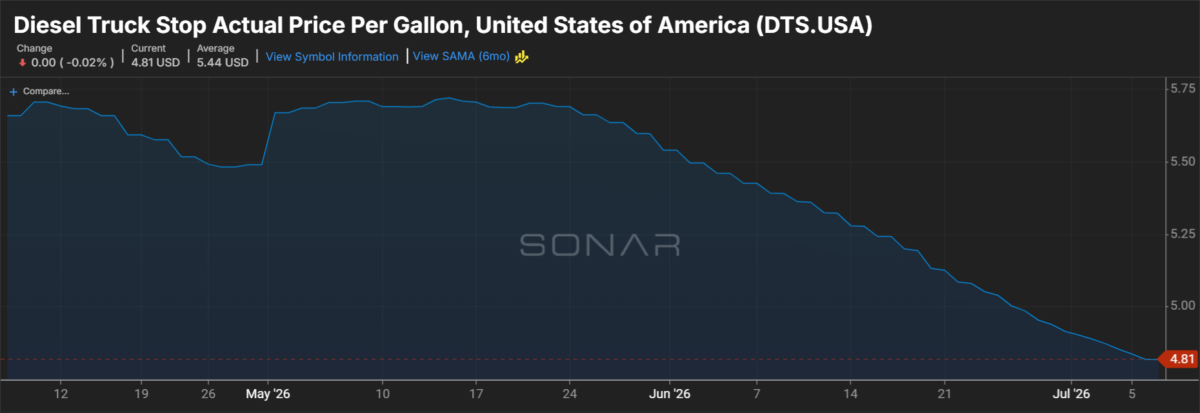

Meanwhile, the DTS.USA data series in SONAR was at $4.81/g Tuesday.

But the more stark “split decision” in the oil market is more clearly evident in what are known as “crack spreads” between the price of crude and the price of the products produced from that crude.

Wild numbers in the 3:2:1

The most basic crack spread benchmark is the 3:2:1 crack spread, which is produced by taking the price of three barrels of benchmark Brent or WTI crude, and subtracting that from the price of two barrels of RBOB gasoline, which is an unfinished gasoline product, plus one barrel of ultra low sulfur diesel.

That crack spread in recent days has been 70% to 75% of the value of a barrel of crude. At the start of June it was about 45%. When 2026 began, it was about 27%.

Part of that has been that even as crude prices have fallen in recent weeks, products have not. Crude on the CME commodity exchange June 23 settled at $77.08/barrel. Monday, the settlement was $71.99/b. Meanwhile, ultra low sulfur diesel on the CMD settled $3.1762/g on June 23, and $3.2984/b Monday.

Factors leading to that are tied to a large degree by the partial reopening of the Strait of Hormuz that has unleashed large quantities of crude on to the global market.

But that rush of crude supplies doesn’t immediately turn them into refined products like diesel and gasoline. The markets for those products are showing signs of having run down inventories globally to keep prices from soaring higher than anticipated when the war between Iran and the U.S./Israel alliance began.

Can’t last forever

The crack spread numbers are so unprecedented that it is leaving analysts few words to describe how bizarre it is. But it has also led to a general consensus that something needs to give. Either the price of crude needs to fall to bring the spread toward some form of normalcy, or product prices need to decline toward a more normal spread against crude.

Amrita Sen, the director of market intelligence at Energy Aspects, said in a CNBC interview that there has been too much focus on the crude number as a sign that the market is headed into a period of prolonged weakness.

One of the reasons crude prices did not soar as much as anticipated after the beginning of the war was China’s role in slowing imports and capping the market from going higher with the gap in China filled by drawing down inventories.

But Sen said market observers looking at the headline number of lower crude prices are missing the fact that “It’s not demand that’s off, it’s (Chinese) crude imports that are down.”

“Our data shows that China has been able to run down that inventory for a good four months now, and now they’re starting to see some tightness,” Sen said.

Dan Pickering of Pickering Energy Partners said in a recent online commentary that there were several reasons for the downward trend in crude prices, which have seen the price of global crude benchmark Brent drop from about $93/barrel a month ago to a settlement Monday on the CME commodity exchange of about $72/b.

He cited four key factors: “The US appears unwilling to return to sustained kinetic actions against Iran; more supply IS moving through the Strait of Hormuz; China has not yet returned to importing crude; the International Energy Agency is warning of a supply glut in 2027.”

But Pickering expressed caution as well, describing the current period as a “honeymoon phase. “The physical side of the oil market remains tight…and eventually supply/demand/inventory dynamics drive the bus,” he wrote.

Pickering said his firm believes that the crude market should be more bullish. “The conundrum is that investors won’t care until prices go up, but prices won’t go up until investors care,” he wrote. “The next 2-3 months will bring plenty of data points to more definitively shape the bull/bear arguments.”

The glut of 2027?

Two to three months brings the oil market closer to 2027. There is an assumption of some degree of normalcy in 2027 forecasts that see the fundamentals of supply and demand pointing toward lower prices, in essence the same imbalance that was predicted for 2026 before the Iran war turned all assumptions upside down.

In an interview on CNBC, Citigroup’s Francisco Martoccia said his company’s forecast is that Brent next year can drop to $60/b “because the geopolitical premium has eroded, while fundamentals remain weak,” he said.

The risk to that model, Martoccia said, would be China coming back into the market as a supplier, and the ending of U.S. supply of oil into the market as it dials back its release of oil from the Strategic Petroleum Reserve. Even if that happens, Martoccia said, Citi’s analyst remains bearish. “We believe the memorandum of understanding between the parties will hold,” he said.

More articles by John Kingston

Montgomery lawsuit likely headed back to Illinois district court

TQL case on broker transparency heads to oral arguments

Highway, post-Montgomery, requiring ELD hookups for all carriers

The post As prices fall, crack spread signals a split in oil markets appeared first on FreightWaves.